Blog

Mar 13, 2026

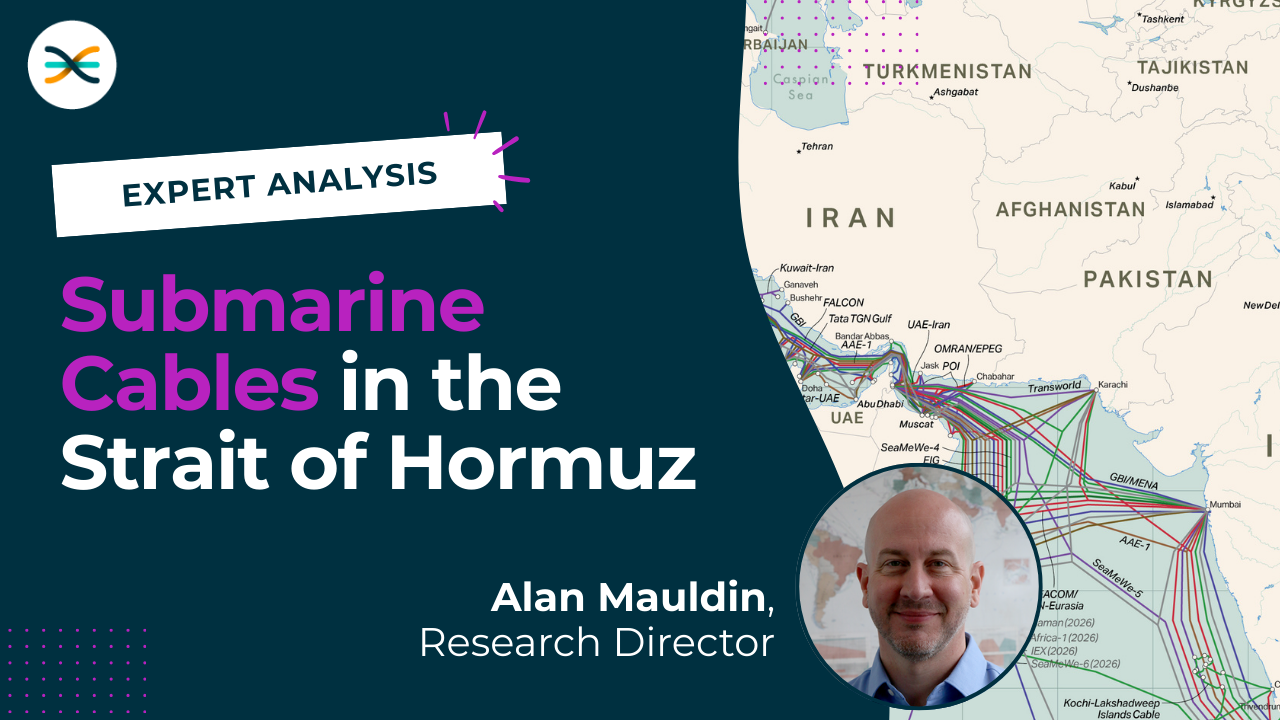

Navigating Hostile Waters: Submarine Cable Infrastructure and the Strait of Hormuz

The Strait of Hormuz is a crucial artery, not only for the transit of oil and cargo but also for the...

What's shaping the trajectory of the global bandwidth market? To answer that question, we identified four significant trends worth watching within our recently updated Transport Networks Research Service.

Here are a few of the most widely-impactful trends shaping long-haul capacity demand and pricing.

The global infrastructure buildout to support AI is unprecedented in its scale. Data center investments currently command the majority of capital expenditure. However, the long-haul networks that facilitate distributed AI workloads are becoming critical as well. The long-term impact of AI on network bandwidth requirements is still evolving and lacks a simple, uniform answer.

We seek to capture the impact of AI in our content provider bandwidth. This category includes many types of companies, including AI platform companies and neoclouds. International content provider bandwidth is expected to increase 9-fold from 2025 to 2035. To meet these demands, major hyperscalers and a new wave of neocloud specialist providers are aggressively acquiring long-haul capacity to interconnect their AI clusters. Autonomous AI agents are expected to intensify bandwidth requirements.

Google is in the midst of a gigantic deployment of new private undersea infrastructure. The company is building a global mesh of 16-fiber pair cables. While Google is the sole owner of these cables, it will not be the only user. The company is selling whole and partial fiber pairs on the cables, but will likely retain the majority of fiber pairs for its own use. Subscribers to our Transport Networks Research Service can view a map of Google's fully and partially-owned cable investment in the platform.

Meta is also significantly investing in private submarine cables. It holds sole ownership of the Anjana trans-Atlantic cable and the planned ORCA trans-Pacific cable. Meta's most ambitious project, Project Waterworth, will consist of multiple cables spanning 50,000 kilometers, linking the United States, Brazil, South Africa, India, Malaysia, and Australia. Transport Networks Research Service subscribers can see a map of Meta's fully and partially-owned cables in the platform.

Google's and Meta’s aggressive cable deployment strategies present telecom carriers and other network operators with a strategic choice: acquire fiber pairs on private content provider cables (if available) or invest in their own new cables. Similar to the approach taken by Google and Meta, Amazon plans to build the company's first private cable—Fastnet—across the Atlantic.

A sizeable share of investment lies in cables owned exclusively by content providers. Out of total new cable investment from 2024-2029, 27% is in private content provider cables. There is also a further 26% that is in cables where at least one content provider is an investor.

New Cable Investment by Ownership Type

While geopolitical concerns have always played a role in determining which companies deploy long-haul networks (and in which locations), several recent developments are reshaping network deployment trends.

As of this writing, war is disrupting activity in the Gulf. As a result, the installation of the Gulf portions of 2Africa and SeaMeWe-6, in addition to the planned FIG cable, are delayed. When installation of these systems can resume is unclear.

Meanwhile, the Red Sea continues to face major problems. The Yemeni civil war had created permitting headaches even before the spate of rebel attacks on commercial shipping vessels. Cable laying vessels require permits to enter a country’s territorial waters. When two different entities claim the same swath of sea, the situation becomes complicated.

These issues have delayed the installation of numerous systems, some of which have been partially deployed except for southern Red Sea segments. These problems with installation, as well as substantial delays in cable repairs in the southern Red Sea, are spurring efforts to develop bypass solutions.

In Asia, cable builders are finding it increasingly difficult to receive Chinese permits for new cable deployment in the South China Sea. The ADC intra-Asian cable finally entered service at the end of 2024, followed by the SJC2 cable in July 2025 after multi-year delays. (SJC2 was originally planned to be in service in Q4 2020!)

To avoid these problems entirely, many new intra-Asian cables such as Apricot, Candle, AUG East, and I-AM Cable are exploring unconventional alternative routes outside the South China Sea to connect Southeast Asia with Northeast Asia. In addition, U.S. government opposition to direct China-to-U.S. cables has boosted the introduction of several cables from Southeast Asia to the U.S. These include Echo and Bifrost.

For all but the very largest users of capacity, leasing wavelengths remains the status quo, as the economies of scale provided by spectrum or fiber pair ownership have remained out of reach. However, higher fiber count cables have the potential to change that by dramatically reducing the cost per bit and making fiber pair ownership far more affordable. Many customers are currently calculating when it makes sense to purchase a fiber pair or spectrum instead of leasing wavelengths. But fiber pair pricing is very cable specific and not subject to the same pricing trends we discussed above.

Content providers have also been increasing their direct ownership in new submarine cables for years. Historically, they have either partnered with service providers in a consortium for those investments or sold fiber pairs to providers, which injected fresh supply and competition into the wholesale market. There are concerns, though, about whether hyperscalers will continue to sell fiber on new systems and if they do, how many pairs per cable will be available. This could potentially limit supply and competition on some routes, curbing price reductions as well.

Despite this, the outlook for the wholesale market is not entirely doom and gloom. Customers are consuming more bandwidth than ever before, particularly with the increasing adoption of cloud services and emerging AI applications. Fulfilling the wholesale requirements for the long tail of capacity users that exists beyond hyperscalers will continue to be a challenging, but critical, business going forward.

Our Transport Networks Research Service delivers data and analysis on long-haul networks and the undersea cable market, with forecasts of international bandwidth supply, demand, prices, and revenues. Learn more and get research samples delivered to your email.

Mar 13, 2026

The Strait of Hormuz is a crucial artery, not only for the transit of oil and cargo but also for the...

Feb 11, 2020

There's been a lot of press about delayed approval for the Pacific Light Cable Network (PLCN) cable,...

Jul 24, 2025

There is no shortage of headlines about high-profile cable breaks, particularly around the Baltic Sea...