Blog

Jun 7, 2023

Latin American Pricing Takeaways From ITW

Last month, the TeleGeography team joined scores of ICT infrastructure professionals in National Harbor,...

What are the latest trends in Latin America’s wavelength market?

We’ve been analyzing trends in the global wavelength marketplace for decades, with data in our Wavelengths Pricing platform going back to 1999. This post provides an in-depth look at Latin America, examining the evolution of connectivity pricing and outlining key topics relevant to wavelength pricing dynamics across the region.

The transport market in Latin America continues to be dynamic. On key routes from hubs like São Paulo, Bogotá, and Mexico City to the United States, high-capacity sales at low per-unit costs are typical. Yet in areas with less demand, less established infrastructure, or more limited carrier competition, 10 Gbps capacities and lower are still common.

Generally speaking, a consistent trend across Latin America is that prices are declining steadily. Across all routes we track connecting the U.S. and Latin America, the weighted median price for 100 Gbps wavelengths fell an average of 20%, compounded annually, from 2022-2025. The weighted median price for 10 Gbps, in comparison, fell just 12% during that same period. Although 10 Gbps is an important product in many markets, we more often see 100 Gbps as the capacity of choice in Latin America. And in the markets where supply and competition are robust, the cost of 100 Gbps has fallen impressively.

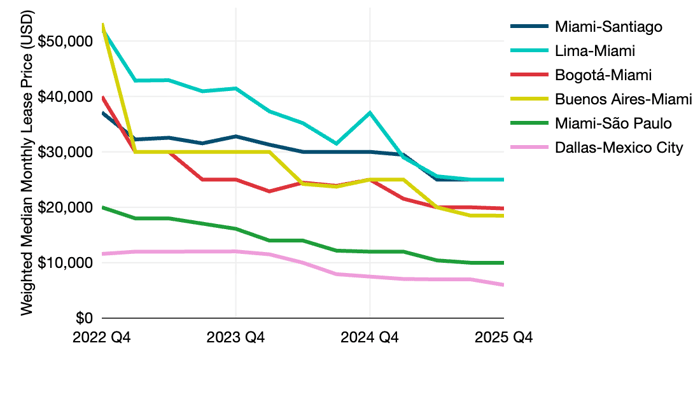

Price erosion remains commonplace across all major routes in Latin America. But the rate of erosion varies by route. The below figure helps us visualize this better by showing recent price decline on key Latin American routes. From 2022-2025, we saw the weighted median price of 100 Gbps on these routes fall an average of 21%, compounded annually.

Weighted Median 100 Gbps Wavelength Prices on Key Latin American Routes

As you can see above, Miami–São Paulo and Dallas–Mexico City continue to be the most competitively priced routes in the region. These are both very established markets where supply, demand, and competition are abundant. One noteworthy difference between them is that Dallas–Mexico is a shorter terrestrial route, which leads to lower costs (and, in turn, lower prices for buyers) than a subsea route like Miami–São Paulo.

Separately, steep price erosion has brought the Buenos Aires–Miami and Lima–Miami routes in line with others in the region. From 2022-2025, the weighted median price of 100 Gbps on Buenos Aires–Miami fell 30%, compounded annually. For Lima–Miami the price of 100 Gbps fell 22% over the same time period. This comes as both markets have seen increased competition and global carriers offering highly competitive prices.

Bogotá–Miami connectivity is also competitively priced and will likely get even cheaper. The weighted median cost for 100 Gbps on Bogotá–Miami in Q4 2025 was down 21%, compounded annually, from 2022.

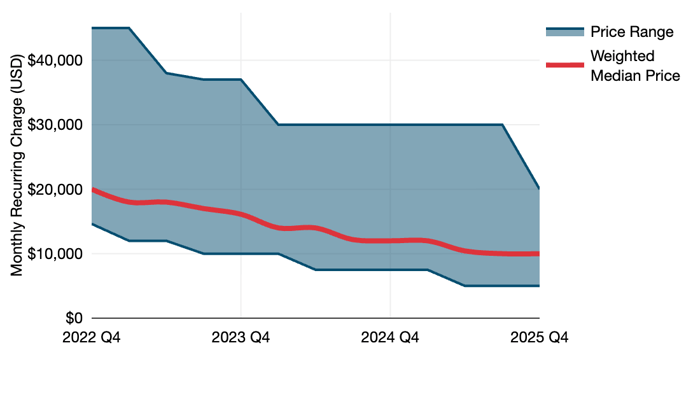

Comparing average prices on different routes is a useful exercise. Similarly, understanding the range of prices on a given route can help reveal deeper dynamics at play. In the below figure we see such a price range for Miami–São Paulo from 2022-2025. Let’s have a look and discuss what the data tell us.

Weighted Median & Price Range for 100 Gbps Wavelengths on Miami–São Paulo

For many years, Miami–São Paulo has been Latin America’s de facto main route for connecting to the United States. As a result, this route has attracted various competitors selling capacity at a range of prices. And over the past few years, the range of prices has stayed relatively consistent. In Q4 2022, the highest price reported to us was $45,000, around three times more than our reported low. That’s nearly the same as in Q4 2025, when our maximum price for Miami–São Paulo of $20,000 was four times the low. Across that three-year span, price decline was faster for the minimum price (-30%) than for the weighted median (-21%) or maximum (-24%). This supports what we’ve heard from contacts in the industry who note that prices on this route have become extremely competitive. Although Miami–São Paulo is a well-established market with high barriers to entry, the price for 100 Gbps transport keeps falling at impressive rates.

After several years of slow growth, Latin America and the Caribbean are beginning to see a wave of new subsea systems bring additional capacity to the marketplace. This includes recently launched cables like Firmina and others like CSN-1, TAM-1, MANTA, TIKAL/AMX-3, CELIA, and Project Waterworth expected to enter service in the coming one to two years. This increased supply will push 100 Gbps prices downward, especially on routes with ample competition. After that, we expect 400 Gbps sales to become more common on established routes with strong demand in the region.

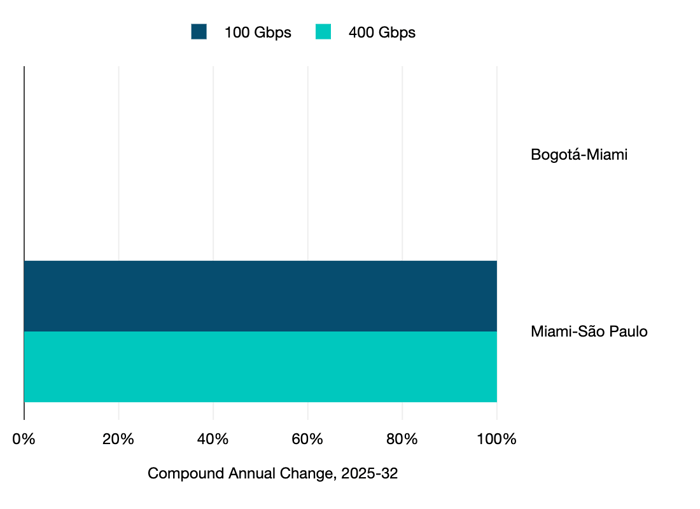

On two such routes, we anticipate price erosion to remain steady in the coming years. On Miami–São Paulo, we forecast 100 Gbps prices to fall 12%, compounded annually from 2025 to 2032. And on Bogotá–Miami we expect erosion to be slightly quicker over that time period at 16%.

Forecasted 100 & 400 Gbps CAGR Price Decline on Key Latin American Routes

Once the 400 Gbps market on these routes is better established, we expect price erosion to outpace that of 100 Gbps. From 2025-2032, we forecast 400 Gbps prices will fall an average of 15% on Miami–São Paulo and 20% on Bogotá–Miami, compounded annually.

Beyond these established markets, we expect prices to continue to fall throughout the region. And in markets where new capacity is expected to come online, higher capacity purchases will become more attractive to customers. For countries like Mexico, that means 400 Gbps sales will become more common. In smaller markets like most Caribbean islands, that will eventually mean 100 Gbps wavelengths are sold more frequently.

You can find this data and analysis and more in our Wavelengths Pricing platform. Take a look at the video tour below. (And you can also check out the other pricing we have available in our Network Pricing Database.)

Jun 7, 2023

Last month, the TeleGeography team joined scores of ICT infrastructure professionals in National Harbor,...

Feb 10, 2022

Anyone familiar with our Pricing Suite knows that São Paulo is Latin America’s de facto center for...

Apr 3, 2024

A few weeks ago, TeleGeography headed back to São Paulo to participate in the Capacity Latin America...